Sales volume increased 47% year over year, with 224 transactions compared to 152 in May last year, marking the busiest May in recent years. However, the average price declined 18%, from $1,478,294 to $1,209,257.While more homes are selling at lower prices, the underlying trends are more complex than the headlines indicate. Let’s take a look at the numbers.

How Did Richmond Hill Real Estate Change Over the Past Year?

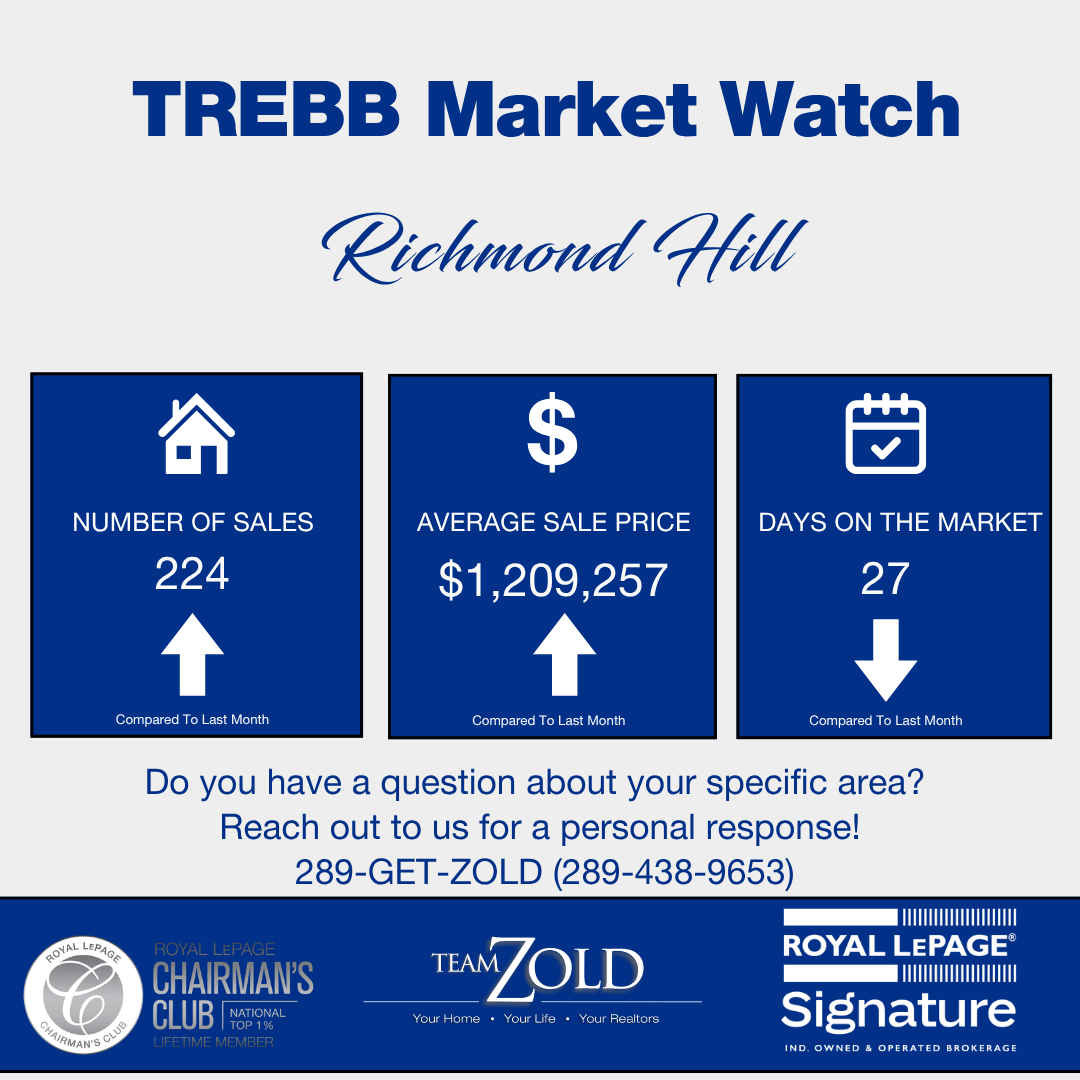

In May 2026, Richmond Hill recorded 224 home sales, up 47% from May 2025, while the average sale price dropped to $1,209,257 (down 18.2% year over year). The median fell 8.2% to $1,165,000. The sale-to-list ratio improved from 97% to 99%, and homes are selling 4 days faster than a year ago.

Here is the full year-over-year comparison:

| Metric | May 2025 | May 2026 | Change |

|---|---|---|---|

| Average Price | $1,478,294 | $1,209,257 | -18.2% |

| Median Price | $1,268,750 | $1,165,000 | -8.2% |

| Total Sales | 152 | 224 | +47.4% |

| New Listings | 757 | 646 | -14.7% |

| Active Listings | 1,191 | 1,030 | -13.5% |

| SNLR | 30.4% | 31.3% | +0.9 pts |

| Average Days on Market | 31 | 27 | -4 days |

| SP/LP | 97% | 99% | +2 pts |

Source: TRREB Market Watch, May 2026

The notable gap between average and median price declines is significant: the average fell 18.2%, while the median declined only 8.2%. This 10-point difference indicates that most of the softening in prices is concentrated in the $2 million-plus segment. Excluding these higher-end sales, the typical Richmond Hill home has decreased by about 8%, which is less dramatic than the average suggests. Buyers in the $1.1 to $1.4 million range are seeing softer prices than last year, but not to the extent implied by the average.

The sale-to-list ratio increased from 97% to 99%. While this may seem unexpected given lower prices, it reflects more realistic pricing by sellers. Last May, homes were listed high and negotiated down, resulting in a 97% ratio. This year, sellers are aligning their prices with market conditions, and buyers are responding accordingly. For a $1.2 million listing, a 99% ratio leaves about $12,000 in negotiating room, which is minimal. Freehold townhouses sold at 103% of asking, above list price.

Sales increased 47% year over year, while active listings declined 13.5%. Average days on market fell from 31 to 27. This indicates that buyers are acting more decisively, driven by improved affordability. Meanwhile, new listings dropped 14.7% from last May, leading to more buyers competing for fewer homes. As a result, the SNLR rose from 30.4% to 31.3%, and SP/LP improved despite lower prices.

What Happened by Property Type in Richmond Hill This May?

Detached homes experienced the largest dollar decline, with the average down 21.1% ($420,182). Condo apartments were most resilient, declining only 6.8%. Freehold townhouses were the most competitive segment, selling above asking at 103% SP/LP and averaging just 22 days on market.

Average Sold Price by Property Type:

| Property Type | May 2025 | May 2026 | Change |

|---|---|---|---|

| Detached | $1,992,959 | $1,572,777 | -21.1% |

| Semi-Detached (8 sales) | $1,244,050 | $1,103,924 | -11.3% |

| Freehold Townhouse | $1,175,040 | $1,059,696 | -9.8% |

| Condo Townhouse (11 sales) | $847,000 | $736,270 | -13.1% |

| Condo Apartment | $611,274 | $569,611 | -6.8% |

Source: TRREB Market Watch, May 2026

Median Sold Price by Property Type:

| Property Type | May 2025 | May 2026 | Change |

|---|---|---|---|

| Detached | $1,620,000 | $1,431,500 | -11.6% |

| Semi-Detached (8 sales) | $1,273,750 | $1,075,000 | -15.6% |

| Freehold Townhouse | $1,201,000 | $1,042,495 | -13.2% |

| Condo Townhouse (11 sales) | $905,000 | $698,990 | -22.8% |

| Condo Apartment | $592,000 | $560,000 | -5.4% |

Source: TRREB Market Watch, May 2026

Detached homes saw the largest decline in dollar terms, with the average price dropping over $420,000 from $1,992,959 to $1,572,777. The median fell 11.6%, from $1,620,000 to $1,431,500. This gap indicates that a few lower high-end sales significantly reduced the average. Most detached buyers are experiencing a notable but less severe correction.

Freehold townhouses stood out this May, selling at 103% of list price with an average of just 22 days on market, the fastest among all segments. The average price was $1,059,696, down 9.8% from last year. This combination of lower prices and above-asking sales indicates strong competition in this price range, as buyers shift from detached homes to townhouses.

Condo apartments remained relatively stable, with the average price down 6.8% to $569,611 and the median down 5.4% to $560,000. Sales volume increased from 31 to 41. Although a smaller segment, condos have been the most price-stable during this correction.

Semi-detached and condo townhouse numbers should be read with caution. Sales of 8 and 11, respectively, are not enough volume to draw reliable conclusions from the averages.

Richmond Hill Market Trends Over the Past 12 Months

| Month | Average Price | Sales | SNLR | SP/LP |

|---|---|---|---|---|

| May 2026 | $1,209,257 | 224 | 31.3% | 99% |

| April 2026 | $1,175,275 | 184 | 29.7% | 97% |

| March 2026 | $1,219,863 | 159 | 29.3% | 98% |

| February 2026 | $1,166,816 | 121 | 28.7% | 97% |

| January 2026 | $1,285,799 | 98 | 28.6% | 96% |

| December 2025 | $1,220,811 | 114 | 28.6% | 97% |

| November 2025 | $1,255,877 | 163 | 29.7% | 97% |

| October 2025 | $1,334,199 | 175 | 29.9% | 98% |

| September 2025 | $1,324,741 | 188 | 30.8% | 99% |

| August 2025 | $1,247,531 | 176 | 30.3% | 98% |

| July 2025 | $1,325,820 | 204 | 30.4% | 98% |

| June 2025 | $1,294,905 | 174 | 30.4% | 98% |

Source: TRREB Market Watch

The highest price in the past 12 months was $1,334,199 in October 2025. Prices declined through winter, reaching a low of approximately $1,166,816 in February 2026, then stabilized between $1.17 and $1.22 million in spring. May’s average of $1,209,257 is about 9% below the October peak.

The SP/LP ratio remained below 100% throughout the past 12 months. It reached a low of 96% in January 2026 and has since increased to 99% in May, matching the strongest level since September 2025. This trend indicates that the gap between seller expectations and buyer offers is narrowing, and market gridlock is beginning to ease.

SNLR reflects a similar trend, bottoming at 28.6% in December and January and rising to 31.3%. While still in buyer's market territory (below 40%), the market is moving toward a more balanced state.

April 2026 vs May 2026

| Metric | April 2026 | May 2026 | Change |

|---|---|---|---|

| Average Price | $1,175,275 | $1,209,257 | +2.9% |

| Median Price | $1,055,900 | $1,165,000 | +10.3% |

| Total Sales | 184 | 224 | +21.7% |

| New Listings | 634 | 646 | +1.9% |

| Active Listings | 1,009 | 1,030 | +2.1% |

| SNLR | 29.7% | 31.3% | +1.6 pts |

| Average Days on Market | 34 | 27 | -7 days |

| SP/LP | 97% | 99% | +2 pts |

Source: TRREB Market Watch, May 2026

Month over month, the spring acceleration is unmistakable. Sales climbed 21.7% from April to May. Average price rose 2.9%, and the median jumped 10.3% from $1,055,900 to $1,165,000. SP/LP improved from 97% to 99%, and days on market dropped from 34 to 27, a full week faster. Listing supply was roughly flat, indicating that the increased activity is driven by buyer demand rather than a surge in new inventory.

This trend is consistent across York Region, with Richmond Hill showing particularly strong momentum in the spring market.

Check out our Richmond Hill April 2026 Market Update post for more information.

What Does This Mean Heading into June?

For Sellers

The market is favouring realistic pricing more than at any point this year. With SP/LP at 99%, homes priced at current market value are selling near asking and moving in under a month. However, pricing at last year’s levels is not advisable. Buyers are active, with 47% more transactions than a year ago, and they are well informed about current values. Price your home appropriately to attract offers; overpricing will likely result in an extended time on the market.

For Buyers

This is an important period for buyers. Sales activity is up 47% from last year, indicating increased competition. Prices remain well below last year’s levels, down 8% on the median and more in the detached segment. With SP/LP at 99%, significant discounting is diminishing; there is still some negotiating room, but less than three months ago, when SP/LP was 96-97%. Freehold townhouses are already selling above asking. If current trends persist, negotiating room will likely decrease further this summer.

What to Watch in June

Monitor two key factors in June. First, check whether SP/LP remains at or above 99%. If it surpasses 100%, it would indicate a shift from a buyer’s market toward a balanced market across all segments. Second, track new listings, which were 14.7% below last May. If this supply constraint continues while buyer activity remains strong, SNLR will rise, and negotiating room will narrow. These conditions suggest a more competitive summer is developing.